Detecting and Preventing Misappropriation of Funds

Detecting and Preventing Misappropriation of Funds

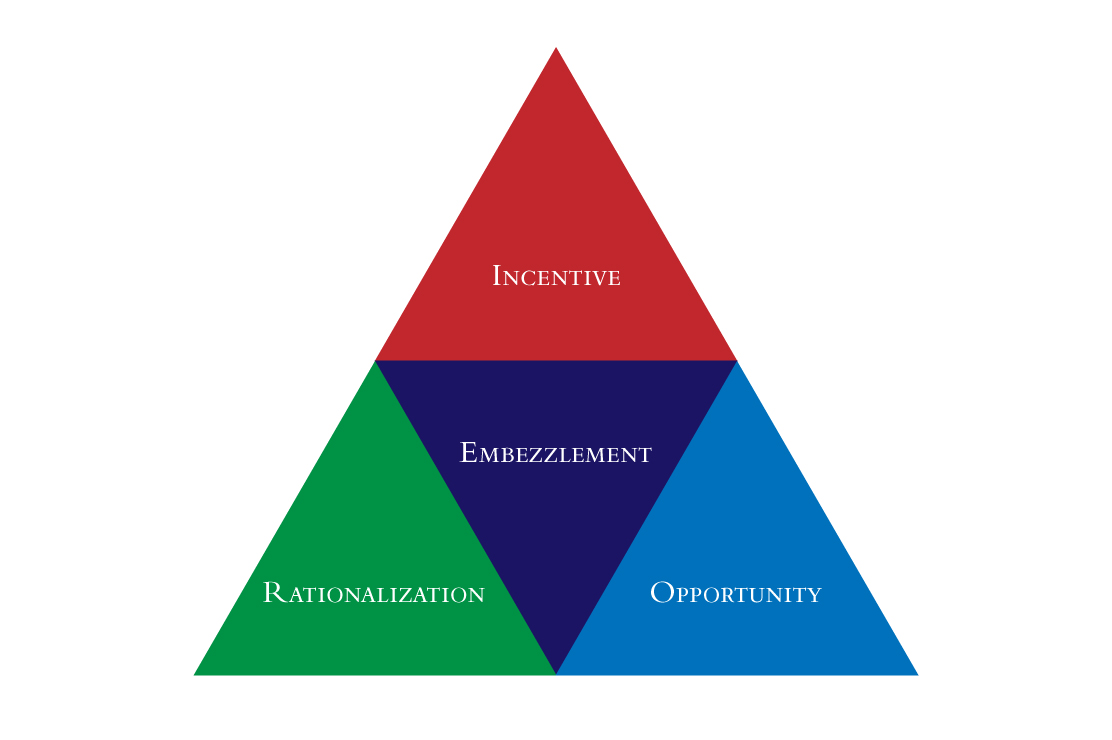

Understanding the Risks: Misappropriation of funds is a serious concern for businesses and organizations of all sizes. It involves the unauthorized or improper use of funds for personal gain or other unauthorized purposes. Understanding the risks associated with fund misappropriation is crucial for implementing effective prevention measures.

Common Red Flags: There are several red flags that may indicate potential misappropriation of funds. These include unexplained or unusual transactions, missing documentation, sudden changes in financial behavior, and discrepancies in financial records. It’s essential for businesses to be vigilant and recognize these warning signs early on.

Implementing Internal Controls: One of the most effective ways to prevent misappropriation of funds is by implementing robust internal controls. This includes segregation of duties, regular audits, strong oversight, and clear policies and procedures regarding financial transactions. By establishing and enforcing these controls, businesses can minimize the risk of fund misuse.

Training and Education: Another important aspect of preventing fund misappropriation is providing training and education to employees. This includes raising awareness about the consequences of fund misappropriation, educating employees about their roles and responsibilities, and promoting a culture of transparency and integrity within the organization.

Whistleblower Policies: Businesses should